The End of Bond Investing? (Not so fast)

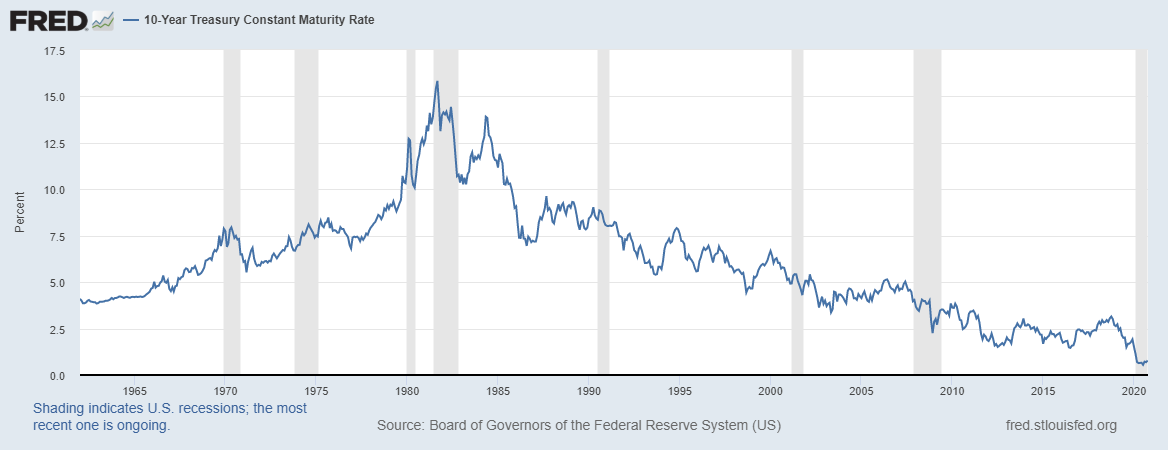

We’ve been talking about the change in interest rates for some time now. But this time, we’ve entered a new period, where the interest you receive on most fixed income investments are at an all time low. Since the peak of rates back in the 1980s interest rates of have been steadily declining, on a long-term basis. Just look at the historic interest on 10-Year Treasuries in the chart below.

If we take a seat, back in Economics class, we remember the relationship of bond prices to interest rates is negative. Meaning, if interest rates go UP, bond prices go DOWN, and vice versa. Hence why we’ve seen, on a long-term average, an impressively bullish environment for bonds. And now the consensus is that that bull run may have just come to an end.

So, what does that mean for us individual investors? Well we’ve talked about it before, but it bears reiterating. This environment makes for a difficult diversification story for more conservative investors, especially those in the income distribution phase of their lives. Net of inflation, the real return on 10-year treasury bonds is negative. Meaning, the interest you collect on those bonds cannot stay ahead of the cost of spending those dollars. And that’s before the downward pressure prices will likely feel in the coming years.

For the past decade, different market analysts have continued to make predictions that we are seeing the end of the bull market for bonds. So far, they’ve been wrong. But even a broken clock is right twice a day, and theirs may have just gotten a fresh set of new batteries. We hate to utter the dreaded words: “But, this time it’s different”, but, well, this time it likely is. With interest rates having no where to go from here, we could be looking at a scenario where the prices of high-quality bonds, think US Treasuries, will start providing negative returns, with little hope of interest keeping total returns positive.

Now that we’ve sufficiently painted the picture of doomsday for bonds, let’s take a couple steps back to reality. We’re far from claiming the end of bond investment. There is one thing though that we can’t argue, and that’s the low interest we currently earn. But we can push back on the new claim that “bonds are for suckers” going forward. This whole situation is very much contingent on inflation heating up. Our thoughts on that are a conversation for another time, and we’ve touched on the subject a bit in the past. Let’s just say, significantly higher inflation is not a foregone conclusion.

That leaves us with strategy. The Fed has bluntly said, we are not raising interest rates for the next few years, and are willing for inflation to run higher. That relieves one of the core pressures on bond prices, a tightening of monetary policy. Making bond investment a bit more palatable in the near term. The strategy for bonds is now one less about potential added returns to the portfolio, and more primarily, one of diversification and risk mitigation. Just think of bonds now as the suspension on an old Cadillac. Without any other parts of the car, you’re probably going nowhere. But all put together, they sure help give that old Caddy a smooth ride.

This will change the use of bonds in a variety of portfolios, from conservative on up. But, for now we are taking a “barbell” approach to bonds. On one side, very high credit quality for stability, and a reach for higher yield on the other. If the theory is correct, this approach should persist for the time being, but we will need to make changes in the future. Those will likely consist of abandoning traditional bond allocations, and looking for bond proxies, like strong dividend yielding stocks and gold.

For now, we are in still the early stages of the game. We have a game plan that will allows us adapt as this potential new environment for bonds unfolds.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. All investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield. Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.